Private equity explained: the beginner FAQ

Private equity is one of the most misunderstood industries in finance. Ask ten people what it is and you will get ten different answers: "the guys who bought Toys R Us", "the investors who own my dentist now", "some kind of hedge fund", "rich people buying companies", "Mitt Romney's old job". All of these are partial, none are complete. This is the beginner FAQ version: the most common questions, answered plainly, with links to deeper explanations where relevant.

What is private equity?

Private equity is a way of owning companies privately (not on the stock market) and trying to make them more valuable before selling them on. A PE firm raises money from large investors, uses it plus borrowed debt to buy companies, works on those companies for 4-7 years, and then sells them for a higher price. For the full version, see what is private equity.

Is private equity the same as hedge funds?

No. Both are "alternative investments" managed by professional firms for institutional investors, but they do very different things.

Hedge funds trade liquid securities (stocks, bonds, derivatives) in public markets. They often hold positions for days, weeks, or months. They aim for absolute returns in most market environments.

Private equity buys whole companies (or controlling stakes), holds them for years, and works to improve them operationally. The work is much more hands-on. The investments are illiquid.

Is private equity the same as venture capital?

No. Venture capital invests in early-stage companies, usually in small minority stakes, betting that a few of them will become enormously valuable. Private equity buys mature companies, usually in majority stakes, using debt to amplify returns. Very different businesses that happen to both be called "funds". See private equity vs venture capital for the detailed comparison.

How do PE firms make money?

Two ways. Management fees (typically 2% of committed capital each year) and carried interest (typically 20% of profits after LPs have received their capital back plus an 8% preferred return). The management fees pay the firm's operating expenses. The carry is where real wealth is created. See two and twenty and carried interest for the detail.

How much do people in PE make?

Analysts and associates: $200-450k all-in. VPs and principals: $500k-1.5m plus carry. Partners: $1-3m in annual cash plus carry that, in a good fund, becomes the majority of total compensation over time. See private equity compensation for the full breakdown.

What is a leveraged buyout?

A leveraged buyout (LBO) is when a PE firm buys a company using a mix of equity (from the fund) and debt (borrowed from banks or private credit). The company itself takes on the debt, not the PE firm. If the company grows or can be sold for more than the purchase price, the debt stays the same and most of the upside flows to the equity. This is the core of how PE generates returns. See the LBO model.

Why do PE firms use so much debt?

Because debt amplifies returns. A deal bought with 50% debt, where the company is sold for 50% more than purchase price, doubles the equity return. Debt is cheaper than equity, and PE firms are structurally good at finding willing lenders. The tradeoff: debt also amplifies downside. A deal that does not work can wipe out the equity entirely.

What is a "portfolio company"?

A company owned by a PE fund. During the ownership period, the company is a "portfolio company" of the fund. The PE firm typically sits on the board, drives strategic decisions, and works with management on operational improvements. See private equity portfolio company.

Who invests in PE funds?

Institutional investors called LPs (limited partners). The biggest category is public pension funds like CalPERS and Ontario Teachers. After that: sovereign wealth funds, insurance companies, endowments, foundations, family offices of wealthy individuals, and a growing share of retail-access products like interval funds.

How do PE firms pick companies to buy?

They look at mature businesses with stable cash flows, room for operational improvement, and clear paths to exit. Common targets include:

- Family-owned businesses where the founder wants to retire

- Corporate divisions being spun off

- Public companies being taken private

- Other PE firms exiting their investments (secondary buyouts)

The "right" target depends on the PE firm's strategy. Some firms specialise by sector, some by size, some by geography.

How do PE firms improve companies?

A mix of financial engineering and operational improvement.

Financial engineering includes taking on debt, restructuring the balance sheet, doing dividend recaps to pull out cash, and using tools like PIK financing, sale-leasebacks, and subscription lines.

Operational improvement includes installing new management, cutting costs, improving pricing, making tuck-in acquisitions, and investing in growth. See private equity value creation for the detail.

In the industry, there is ongoing debate about how much of typical PE returns come from genuine operational improvement versus financial engineering and multiple arbitrage.

How does a PE firm exit a deal?

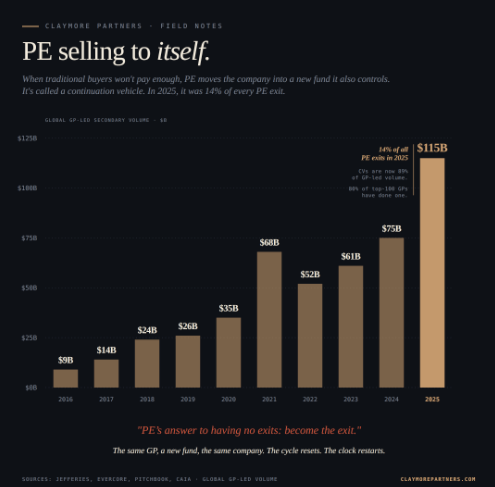

Four main paths. Sale to a strategic acquirer (an industry buyer). Sale to another PE firm (secondary buyout). IPO (taking the company public). Or a continuation fund (selling to a new fund the same PE firm raises). The choice of exit depends on company size, market conditions, and PE firm preference.

Why do people criticise PE?

Several reasons.

Leverage creates risk. PE-owned companies can go bankrupt if they cannot service their debt, which has happened repeatedly (Toys R Us being the famous example).

Fee structures concentrate wealth. The two and twenty model and carried interest produce enormous wealth for a small number of senior partners.

Short-term focus. PE firms usually sell within 4-7 years. Critics argue this incentivises short-term optimisation over long-term value.

Impact on workers. PE-owned companies often reduce headcount or move operations, as the new owners pursue cost reduction.

Healthcare and housing concerns. PE ownership of hospitals, nursing homes, and residential real estate has generated specific controversies about service quality and tenant treatment.

What do PE supporters say?

Several counterarguments.

PE creates value through improvement. Real operational work happens. Many PE-owned companies are stronger at exit than at entry.

PE allocates capital efficiently. Moving underperforming assets from weaker owners to stronger ones is economically valuable.

PE returns beat public markets, historically. Over 30 years, PE has generated 3-5 percentage points of annual premium over public market indices (though this premium is compressing).

Workers and communities often benefit. PE-owned companies often grow faster than their peers, creating net jobs over the investment period.

Both sides have merit. The truth varies wildly by specific deal, sector, and firm.

Is PE a good career?

For the right temperament, yes. High compensation, interesting work, access to senior decision-makers. But also: long hours, competitive culture, long vesting periods on the real wealth, limited exit paths if you want to leave the industry. See private equity compensation for the economics.

What is a "GP" and an "LP"?

GP = General Partner = the PE firm that manages the fund. LP = Limited Partner = the investors in the fund. The GP makes investment decisions and charges fees. LPs commit capital and receive distributions.

What are PE firms called "General Partners"?

The legal structure of a PE fund is a limited partnership. The fund itself is a partnership. The GP is the partner with management control and unlimited liability. The LPs are passive investors with limited liability (they can only lose their committed capital, not more).

How much money is in PE globally?

Roughly $8 trillion of assets under management globally as of 2024-2025, across buyout, growth, venture, secondaries, real estate, and infrastructure. Pure buyout PE (the classic "PE" most people mean) is about $3-4 trillion of that.

Should I invest in private equity as an individual?

For most individuals, access to institutional-quality PE funds requires either substantial wealth (family office territory) or connections. Retail-access products (interval funds, BDCs, evergreen structures) exist but usually have higher fees and less favorable terms than institutional funds. Do careful diligence before committing.

Who runs the biggest PE firms?

In rough order by AUM: Blackstone, KKR, Apollo, Carlyle, Ares, CVC, EQT, TPG, Advent, Bain Capital, Thoma Bravo, Vista. Each has distinct strategies, sector focuses, and cultures.

Why does PE keep growing?

Because LPs keep allocating. Despite fee concerns, illiquidity, and concentrated returns, public pension funds and sovereign wealth funds need returns that public markets have not reliably produced in the past decade. PE has been a consistent source of excess return, at least historically. Whether that continues is an active debate.

The closing take

Private equity is large, complex, controversial, and misunderstood. The basics are simpler than the mythology suggests: raise money from institutions, buy companies with debt, improve them, sell them. The details are where the real story lives: what "improve" means, who benefits, who bears the risk, and whether the whole system produces value or mostly redistributes it.

For the full deep-dive, start with what is private equity. For the mechanics, see the toolkit. For the opinion and commentary, the rest of Not Very Private Equity is where we keep the opinions.