The Eight-Year Hold: Private Equity's $4 Trillion Backlog Is Now an Operating Problem

The deal was underwritten for five years. The company is still here in year eight. Almost nobody planned for the difference.

Private equity used to run on a five-year clock. Buy the company, fix the obvious things, ride the multiple, sell. In 2026 that clock is broken: the average hold has stretched to nearly eight years, some four trillion dollars of portfolio companies are waiting for an exit that keeps not arriving, and Apollo is telling conference audiences to brace for a sharper divide in returns. Most of the commentary treats this as a fund-level liquidity story, which it is. But inside every one of those stranded deals is a company that was underwritten for a five-year plan and is now living through year six, seven or eight of it, with a tired management team, an expired value-creation plan and an incentive scheme that paid out on paper years ago. The backlog is not just a distributions problem. It is an operating problem, and the firms that treat it that way will be the ones selling out of it first.

The clock broke: what the numbers say

The clearest statement of the problem came from inside the industry. At SuperReturn in Berlin in June 2026, Apollo's deputy global head of private equity put the backlog of unsold assets at roughly four trillion dollars and said average hold times have doubled, from around four years historically to almost eight today. His conclusion was not that the market will rescue everyone. It was the opposite: expect a sharper divide in returns between the funds that can sell at their marks and the funds that cannot.

The durable data says the same thing more politely. Bain's Global Private Equity Report 2026 has buyout holding periods at exit hovering around seven years, against the five to six that held through 2010 to 2021. Almost 40 percent of all PE-owned companies are now held for more than five years, up from 29 percent in 2019. This is not a tail of unlucky deals. It is approaching half the asset class.

| Metric | Then | Now |

|---|---|---|

| Average hold at exit | 4 to 6 years (2010 to 2021) | 7 to 8 years |

| Companies held more than 5 years | 29% (2019) | ~40% |

| Distributions as share of buyout AUM | ~14% (ten-year average) | ~6% |

| Five-year rolling buyout DPI | long-run norm | lowest recorded level |

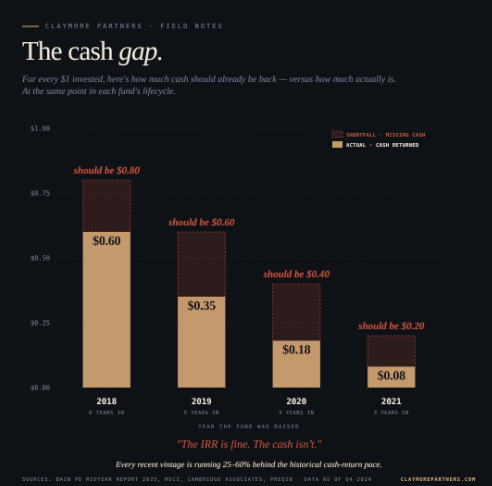

The cash consequence follows directly. Distributions are running at roughly 6 percent of buyout assets under management, against a ten-year average near 14 percent, and five-year rolling buyout DPI sits at its lowest recorded level. The hold is the cause; the DPI drought is the symptom. Limited partners are not waiting for the IRR argument. They are waiting for the money.

Why everything is stuck

Three forces jammed the clock at once. The first is the 2021 and 2022 vintage problem. Companies bought at record prices on peak multiples carry marks that only make sense at tomorrow's hoped-for valuations. Selling now crystallises the gap between the carrying value and what a buyer will actually pay, so sponsors hold and hope instead.

The second is the exit environment itself. The IPO market is quieter, the gap between buyer and seller expectations stays stubbornly wide, and debt now costs real money. The financial tailwinds that used to bail out average operating performance, cheap debt and expanding multiples, no longer exist. A deal that needed the exit maths to work has nowhere to go.

The third is that the squeeze has become visible at fund level. In early June, Partners Group capped withdrawals from one of its evergreen vehicles after redemption requests nearly doubled its gate. The liquidity strain that began in private credit is now knocking on private equity's door, and LP patience, not deal supply, is becoming the binding constraint.

None of these forces resolves the others. A sponsor can wait out the rate cycle but not the vintage problem, and an LP can tolerate one fund's frozen distributions but not a portfolio of them. The stand-off holds until something changes inside the assets themselves, which is precisely why the backlog has stopped being a market-timing question and become a management one.

What year eight does to the deal maths

Time is not neutral in a private equity model. IRR decays with every year that passes while the mark stands still, because the same eventual profit gets spread across more years. MOIC and IRR drift apart until one of them is telling a story the other contradicts: a fund can show a respectable multiple on paper while its annualised return quietly sinks toward what an index fund would have paid without the illiquidity.

The incentive damage is worse and discussed less. Management incentive plans were built around a year-five exit. Options cliff-vested on schedule, the MIP was modelled to pay out at a valuation event, and that event never came. The team that signed up for one sprint has now run two, and the equity that was supposed to make them owners has become an IOU with no date on it.

Then there are the deferred decisions, which compound the way unpaid interest does. Capex postponed until closer to exit. Pricing left untouched because nobody re-prices during a sale process. The second product bet never made. An asset managed for an imminent sale for four consecutive years has been quietly starved, and the starvation shows up exactly when a buyer finally arrives to diligence it.

Year six inside the portfolio company

From inside the company, the long hold has a texture the fund-level commentary never captures. The original value-creation plan expired somewhere around year three. What replaced it is usually a budget, not a thesis: targets without a story, reporting without a destination.

Leadership fatigue is real and measurable. The CEO is on their second CFO. The board pack has stopped asking the growth question and started asking the covenant question. The best operators read the situation correctly and leave for deals with fresher equity, which means the companies that most need operating talent in year six are the ones least able to retain it.

This is the quadrant where Apollo's sharper divide actually gets decided. The companies that exit the backlog first will not be the ones with the most patient banker. They will be the ones that still have a growth story a buyer can underwrite, run by a team that still has a reason to care.

The Year-Five Reset

Any deal past its original underwriting horizon needs a named, ordered agenda. Here is ours.

- Re-underwrite the thesis. Treat year five like a new acquisition. What is the business actually worth today, to whom, and on what story? If the honest answer is unchanged from the 2021 deck, the work has not been done.

- Write a second value-creation plan. The first VCP expired. The long hold needs its own plan, built on operating levers such as pricing, retention and channel mix rather than exit grooming.

- Reset the incentive scheme. Re-strike or top up management equity so the team running years five to eight has years five-to-eight economics, not the ghost of a 2021 option pool.

- Reinvest in the growth engine. The capex and commercial bets deferred until exit are now the difference between a process and a pass. Many sponsors bring in operating partners or embedded growth-execution specialists for exactly this phase: in-house operating teams, fractional executives, or growth-execution firms such as Claymore Partners, alongside the company's own bench.

- Run exit-readiness as a programme, not an event. Clean data, a defensible forecast and proof points a buyer can verify are years in the making, not weeks. Start the programme the day the hold passes its underwriting horizon.

The selection effect: who gets out first

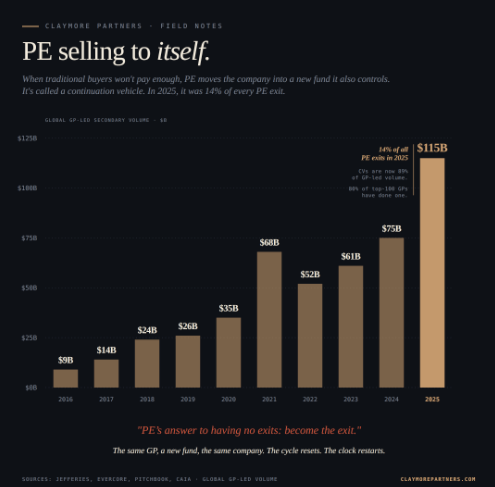

Reframe the sharper divide and it stops being a prediction and becomes a sorting mechanism. The backlog will not clear evenly. Buyers will cherry-pick the operationally fit assets at honest marks, and everything else will roll into continuation vehicles or keep waiting. Four trillion dollars does not exit through a window that narrow without a queue forming, and position in that queue is earned operationally.

Continuation funds are the pressure valve, not the cure. A continuation vehicle moves the asset and prints a distribution, but it does not change what the company earns. The honest test of whether an asset should roll or sell is an operating question, and we built a test for it: if the remaining value-creation runway is real, roll it with a funded plan; if it is not, take the honest price.

Step back far enough and the eight-year hold completes a conversion that has been underway for two decades. Private equity's operational era was a thesis about where returns come from. The backlog makes it compulsory. When you cannot trade your way out, you have to build your way out, and the firms that staffed for building will be the ones whose year-eight companies still look like year-three companies to a buyer.

FAQ: holding periods and the exit backlog

What is the average holding period for a private equity investment?

Historically private equity firms held portfolio companies for around four to five years before selling. That has lengthened sharply: by 2026 the average hold time had roughly doubled to almost eight years according to Apollo, and Bain's Global Private Equity Report 2026 puts buyout holding periods at exit at around seven years. Almost 40 percent of all PE-owned companies are now held for more than five years, up from 29 percent in 2019.

Why are private equity firms holding companies longer than before?

Three forces are at work. Companies bought in 2021 and 2022 were acquired at record valuations, so selling them today would often crystallise a loss against their carrying value. The exit environment has been weak, with a quieter IPO market, a wide gap between buyer and seller price expectations, and debt that costs far more than it did when the deals were underwritten. And because exits are hard, distributions have slowed, leaving funds holding assets while they wait for conditions to improve.

What is the $4 trillion backlog in private equity?

The backlog refers to the roughly four trillion dollars of portfolio companies sitting unsold in private equity funds, waiting for an exit. Apollo's deputy global head of private equity described the overhang at the SuperReturn conference in June 2026, warning that sponsors face growing pressure to return capital to investors and that the industry should expect a sharper divide between funds that can sell their assets at carrying value and those that cannot.

What does a longer holding period mean for private equity returns?

A longer hold mechanically erodes IRR, because the same eventual profit is spread over more years. It also widens the gap between paper metrics and realised cash: a fund can show a healthy multiple on invested capital while having distributed very little. For management teams, longer holds often mean incentive plans designed around a year-five exit no longer motivate, and for the company itself, investment decisions deferred in anticipation of a sale can quietly compound into underperformance.

How do private equity firms manage companies during longer holds?

The better ones effectively re-underwrite the deal: they reassess what the business is worth and to whom, write a second value-creation plan focused on operating levers rather than exit grooming, refresh management incentives so the team has real economics for the extended period, and restart the capital and commercial investments that were deferred when a sale looked imminent. Continuation funds are also used to extend ownership formally, moving the asset into a new vehicle and giving existing investors the option to cash out.

Related reading: What is a NAV loan.